.gif)

Key Takeaways

Running a restaurant can be both a very profitable and rewarding endeavor, as well as a potentially risky one. If you’re a restaurant owner, you want to be sure that you have your bases covered in case something goes awry. You never know when something might happen that suddenly results in a major financial loss.

Considering the extent to which these problems can impact your business, you need to be as prepared as possible before problems arise. The worst case scenario would be allowing your restaurant to go into bankruptcy, which can be the result of poor hiring decisions, failure to adapt to changing circumstances, or other mistakes that you don’t correct in a timely manner.

This article will lay out steps that you can take to help you reduce financial risks to your restaurant and not let your business go bankrupt.

6 Steps You Can Take to Protect Yourself

Running your restaurant efficiently and enthusiastically is an obvious first step to take. In addition to simply maintaining good policies with regard to staffing, inventory, marketing, etc, you should prepare yourself for what might happen if a major problem occurs that carries potential financial losses.

Identify Problems and Map Solutions

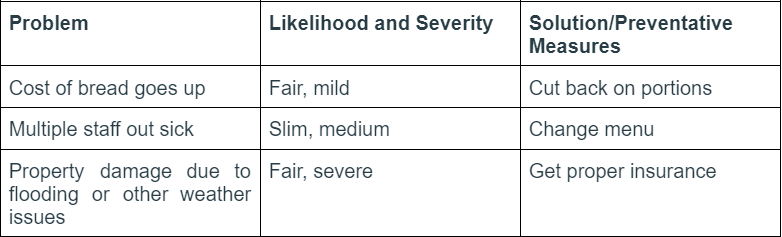

Having a clear picture of potential risks is critical. One preventative measure that you can take is to map out all of the types of problems that might occur which could cause serious financial losses and put them into categories in terms of severity.

In order to do this, you should, first of all, take into consideration that problems can take different forms. They can have both direct and indirect causes, as well as different degrees of effects. This can include everything from the cost of food items to rent increases to preventative measures to ward off natural disasters.

Once you’ve done this, create a probability scenario with different degrees of likelihood, and what preventative measures/solutions you would provide for each of them. For example

When you have a list of potential issues and their respective degrees of severity, you can start thinking about the strategies that you will create to either avoid or manage these problems if they arise.

Manage Your Cash Flow

Proper cash flow management is one of the cardinal rules of restaurant ownership. Regardless of whether or not you face serious problems, you want to have your finances in order so that you can pay staff, take care of your facility, manage food inventory, and plan sales goals.

Optimize Fixed And Variable Costs

Another thing that you should keep in mind is that there are different categories of costs involved in running a restaurant. In general, the kinds of costs that restaurants incur fall into two categories: fixed and variable.

Fixed costs include things that don’t change on a monthly basis, such as the cost of rent and (likely) utilities. Variable costs include things that are out of your control, such as the cost of food, personnel expenses, and your own personal salary. When you create your cash flow scheme, keep these categories in mind so that you can be on the safe side if your variable costs end up being on the high side during particular months.

You can make changes to your fixed costs even though they may seem uncontrollable. If your utility bills are high, consider switching to alternative energy sources like solar power. Research the potential savings and benefits of solar electricity, including the ability to store energy. Plan ahead for replacements of items like dishes and decorations by purchasing them in bulk to save money per item. Similarly, you can partially control variable costs by buying certain food items in bulk or opting for cheaper brands, adjusting staff shifts and overtime, and finding ways to maximize their benefits within your budget.

Similarly, you can control variable costs to some extent by buying certain food items in bulk (or choosing cheaper brands), adjusting staff shifts and overtime allotments, etc. Whatever variable costs you have, think about ways that you might be able to adjust them to maximize their benefit without exceeding your budget allotments.

How Can You Optimize Your Cash Flow?

Here are some of the most important tips to optimize your cash flow:

- Keep close track of your customer data by creating monthly POS reports. Utilizing the right software to create detailed reports of sales data can help restaurateurs analyze and plan their future plans by determining trends (hourly, employee-based, menu-based, inventory-based, etc). It is also a good idea to keep track of your credit card fees as you might be able to modify them by making different kinds of payments.

- Once you have a few months of data to work from, try creating projected monthly cash flow statements based on the data you’ve already compiled. In continuing to analyze your reports, month-by-month, you should gain a better idea of what your projected cash flow will be.

- To truly have a grasp of your restaurant’s business dynamics, you should create profit and loss statements, or statements of your income and expenses. These will help you understand your restaurant’s costs that are subtracted from sales, which will help give you a better idea of your overall financial health. It will not show you particular debts, such as credit card debts, but rather give you an overall impression of the direction your business is heading in.

- Consider hiring temporary staff for particularly busy times of the year.

Keep Track of Your Business Credit Score

As with your personal credit score, your business credit score reflects the degree of financial trustworthiness that your business has earned throughout the course of its functioning.

Business credit scores generally fall into three different ranges: high risk, medium risk, and low risk. The general breakdown is the following:

- High risk - if you receive a score of under 40, your business is considered high risk. This means that you are not considered a good candidate for financial loans, and you will likely have to put out more upfront to secure them.

- Medium risk - If you receive a score between 40-80, you are considered medium risk. This means that you may receive the financing you ask for, but you might be required to submit additional information to prove your financial reliability.

- Low risk - if you receive a score over 80, this is the best position to be in. You will be eligible for more loans with lower interest rates.

What Is Your Business Credit Score Based Upon & And How You Can Improve It

Your restaurant business score is based on different aspects of your business-related activity. This includes the following elements:

- The type of tax accounts you file, whether you are an SME sole trader or a limited company. You should make sure that you submit full returns, rather than abbreviated ones.

- Whether you have paid all your bills on time

- Whether you have been subject to county court judgments or insolvency proceedings

Score calculations are mathematically complex; they aren’t a matter of simply paying some number of bills on time and expecting your score to go up. Therefore, it is best to try to stay on top of your financial obligations all the time so that you can be sure to keep your score up.

Specific things that you can keep in mind to ensure a high score include the following:

- Higher revenue will help improve your score. If you do a good job of building your business, it will be reflected in your score.

- Similarly, longevity will earn you points. The longer you stay in business, the more reliable you will be in the eyes of the credit bureaus.

- Choose vendors that you know make reports to the credit bureaus and be sure to establish good relations with them. Not all vendors do this, so make it part of your research in advance.

- Consider the value of your assets. If your real estate itself has a high value, this will lend you credibility.

Remember that, although they are technically separate, your credit history might play a role in your ability to receive business funding afterward. If you have outstanding debts or a low credit score for other reasons, work on building that up so that it will help your business.

Keep up With Changing Customer Preferences

You can do your best to keep your customers happy with an existing menu, but you can’t control your customers’ preferences all the time. Sometimes new food trends come about that all the local restaurants want to get in on. Or perhaps seasonal changes come about that make people want to try certain things. For example, many people are switching to the Keto diet these days. If you want to keep up with the other restaurants in your area and appeal to this demographic, take the time to study what this diet entails and create some dishes that adhere to its parameters.

What you can do is read up on changing food trends as much as possible to try and stay abreast of changing trends in the restaurant business. If you try something out and it’s not a huge hit with your customers, you can adjust or take it off the menu. But it’s good to try to stay up with the times.

Consider Supply Chain Risks

There are many different ways that supply chain risks can jeopardize all types of businesses. The recent grain blockade in Ukraine disrupted supply chains and drove up bread prices globally.

While it is very difficult to plan for something like the effects of a blockade or other major global issues, restaurants can take into consideration what various levels of supply chain disruptions could do to some of their food supplies and do their best to plan accordingly. This can include taking such measures as diversifying suppliers, maintaining a “buffer” inventory, and also creating backup plans if certain products become unavailable.

Deal With Workforce Disruption

Another potential danger that can happen to businesses if a large number of employees suddenly become unavailable. In cases like this, you will often be forced to shift gears quickly and improvise. Some of the things you could do to make up for staff shortages include:

- Trimming down your menu. If circumstances become difficult, you can still offer top-notch service to your customers; you might just have to limit the options a bit.

- Cross-train your staff. While you might not be able to make waitresses into cooks, there are certain things that you can train your staff to do that will help make operations more efficient in times of staff shortages. Taking orders, handling waiting customers, and other things can be done by alternative staff members to keep operations running smoothly.

- Automate certain tasks. Thanks to advanced technology, more and more things can be automated these days. Electronic menus, payment systems, and reservation systems are just a few of them.

Whatever the issues, you should make sure that the changes you make are wise ones and don’t force you to compromise on food safety, other public health-related standards, or anything else that could endanger your customers or potentially drive them away.

Conclusion

No one can ward off potential financial problems completely. There are certain risks that are part and parcel of running a restaurant. But you can do your best to foresee potential risk scenarios and prepare yourself and your staff for them accordingly. The more you prepare, the lower your risks will be.

Frequently Asked Questions

Key financial risks include fluctuating food costs, labor expenses, cash flow problems, and unexpected events like economic downturns or pandemics.

You can manage risks by maintaining a strict budget, diversifying revenue streams (e.g., delivery, catering), and investing in restaurant insurance for added protection.

.jpeg)

.webp)

.svg)

.webp)